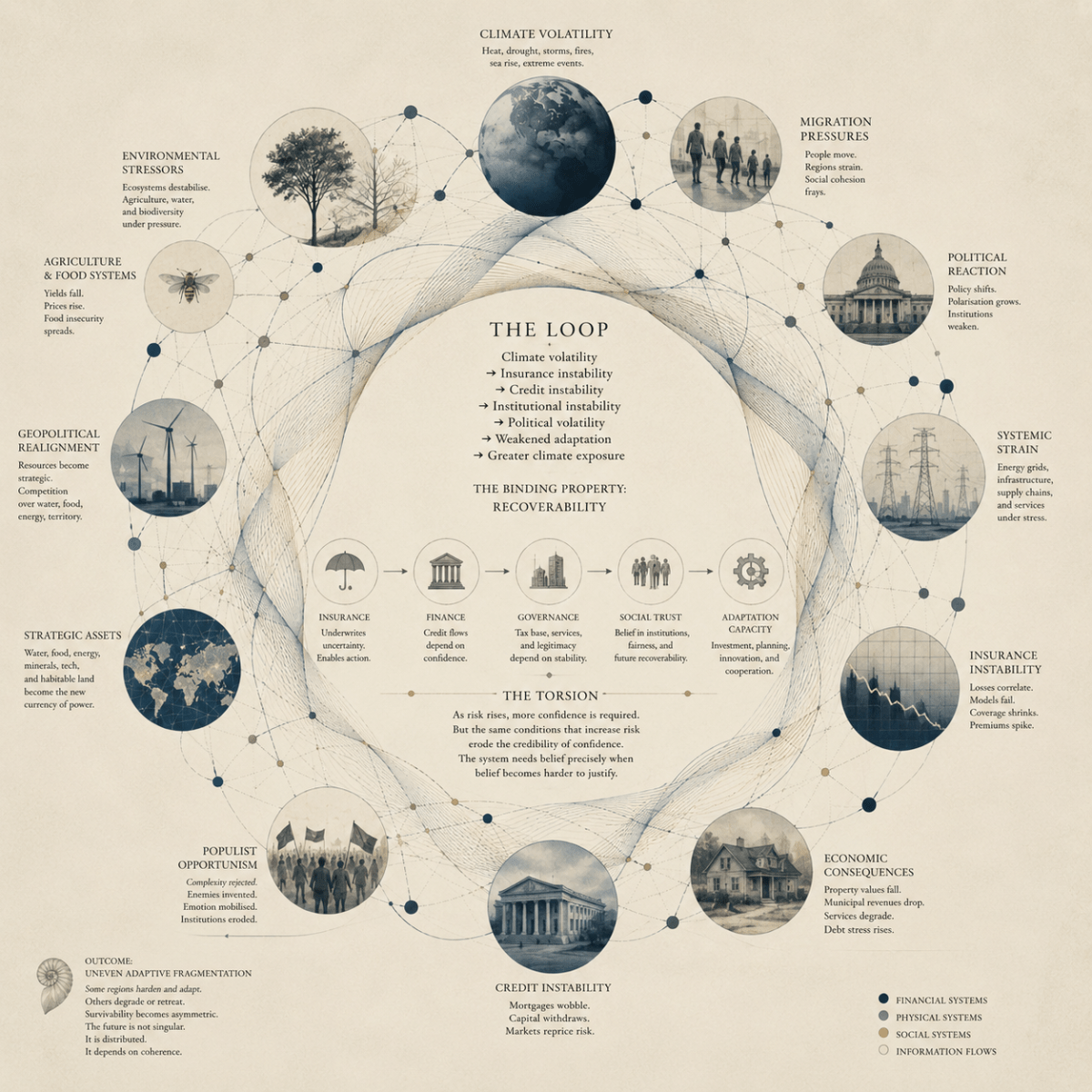

Climate change is no longer an isolated environmental problem. It acts upon every interconnected system simultaneously because modern civilisation is tightly coupled through energy, logistics, finance, infrastructure, agriculture, communications, and governance. Heat alters agriculture. Agriculture alters migration. Migration alters politics. Politics alters energy systems, borders, infrastructure spending, and institutional trust. The systems are not separate. They recursively condition one another. What appears as a weather event in one domain reappears elsewhere as inflation, displacement, insurance withdrawal, political extremity, or strategic instability. The crisis propagates not linearly but relationally, moving through dependency pathways already embedded within the global system.

Insurance is one of the hidden stabilising mechanisms inside this arrangement because it underwrites recoverability itself. Insurance allows uncertain futures to remain economically actionable. Banks issue mortgages because assets are insured. Governments maintain tax expectations because property retains value. Corporations invest because catastrophic loss remains statistically absorbable. Insurance therefore functions less as a financial product than as a distributed confidence structure underwriting continuity across the social field. The deeper binding property is not capital but belief that loss remains containable within institutional time horizons.

This system depends upon disasters remaining partially independent. The mathematics becomes unstable when catastrophes correlate across multiple domains simultaneously. Fires, floods, storms, heatwaves, crop failures, migration surges, infrastructure strain, energy volatility, and geopolitical instability increasingly interact rather than occurring in isolation. Correlated shocks reduce the system’s buffering capacity because losses compound faster than recovery mechanisms can absorb them. The critical antisymmetrical coupling emerges here: as systemic risk increases, societies require greater confidence to preserve coherence, yet the same conditions generating risk simultaneously erode the credibility of that confidence.

Once insurance becomes prohibitively expensive or withdraws from entire regions, secondary consequences propagate rapidly through the surrounding architecture. Uninsured property destabilises mortgage markets. Mortgage instability weakens housing values and municipal revenues. Reduced revenues degrade infrastructure maintenance and public services. This weakens confidence further, accelerating capital withdrawal and political dissatisfaction. The climate crisis therefore manifests economically and institutionally before it appears as outright physical uninhabitability. A burned suburb becomes not merely a local tragedy but a signal transmitted through banking systems, actuarial models, bond markets, electoral systems, and strategic planning frameworks.

Geopolitics consequently reorganises around survivability rather than merely ideological competition. Water access, food production, electrical stability, shipping corridors, semiconductor fabrication, energy infrastructure, and thermally viable territory become strategic assets. States increasingly compete to preserve continuity under conditions of rising systemic stress. Regions previously considered peripheral may become valuable, while historically prosperous regions may become liabilities due to thermal exposure, water scarcity, or insurance instability. The map itself changes meaning. Geography ceases to be passive terrain and becomes an active thermodynamic variable within economic and strategic calculation.

Populism thrives under these conditions because complex systemic explanations are cognitively and emotionally difficult to process. Populist movements compress distributed structural anxiety into simplified symbolic narratives involving enemies, betrayal, corruption, invasion, or restoration. These narratives temporarily stabilise collective emotion while often worsening the underlying conditions through institutional erosion, short-term extraction, antagonistic politics, and epistemic fragmentation. Complexity requires distributed trust and delayed coordination. Populism offers immediate psychological closure instead. The instability therefore recursively amplifies itself through the communicative system, converting systemic tension into emotionally transmissible symbolic conflict.

The likely outcome is not singular collapse but uneven adaptive fragmentation. Some regions will harden infrastructure, redesign cities, construct thermal buffering systems, and maintain partial stability through wealth, technology, and energy access. Other regions will experience recurring degradation, managed retreat, infrastructural exhaustion, insurance failure, or administrative drift. The decisive variable becomes not climate severity alone but whether societies can preserve enough institutional coherence, distributive capacity, and collective trust to continue coordinating recovery across increasingly coupled crises. Climate stress does not create interdependence. It reveals the interdependence that was always already there, exposing civilisation as a system borrowing stability from itself across time until the accumulated debt of coordination begins demanding repayment.

Categories

insurance industry: climate, consequence, catastrophe

Climate change becomes civilisational risk when insurance can no longer translate catastrophe into recoverable cost.